আরও দেখুন

26.03.2026 03:43 PM

26.03.2026 03:43 PM

See also: InstaTrade trading indicators for EUR/GBP

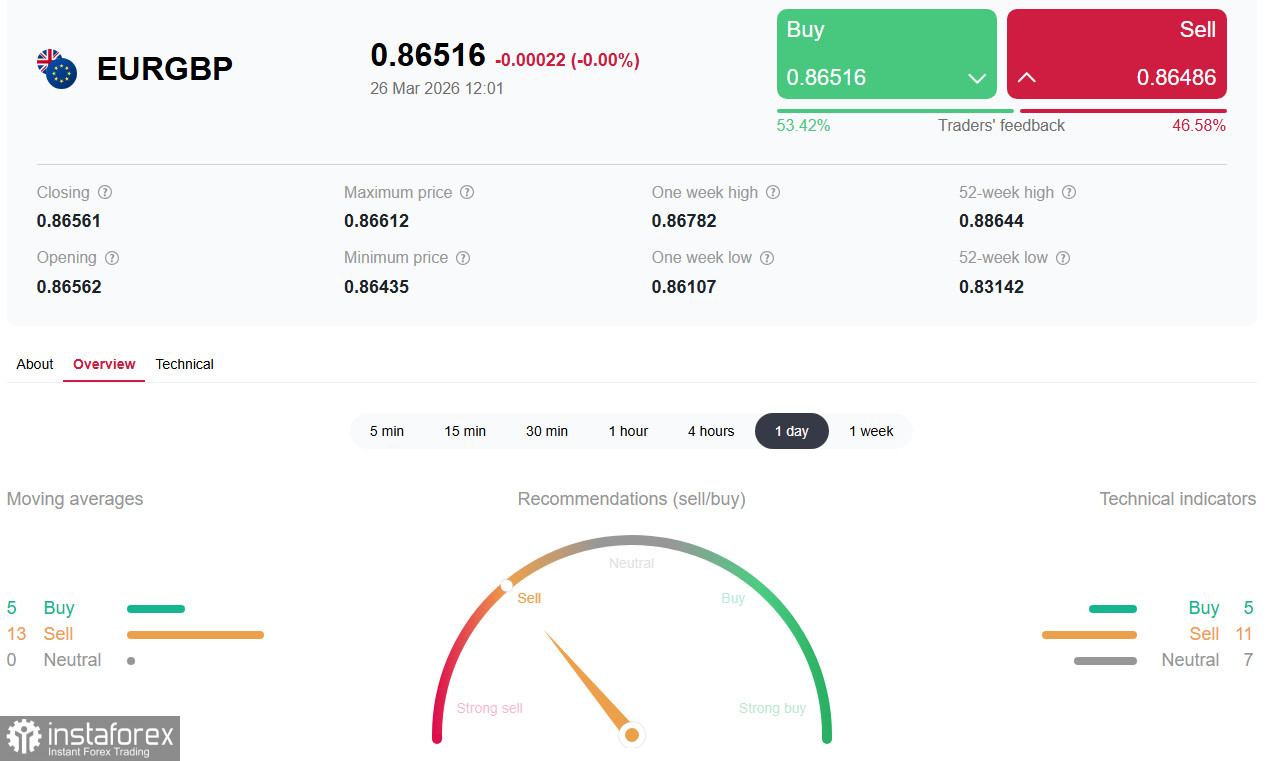

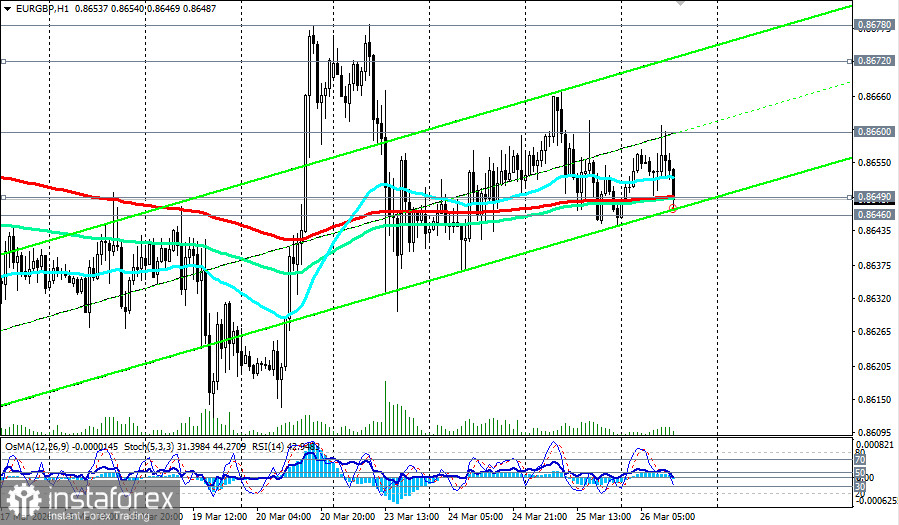

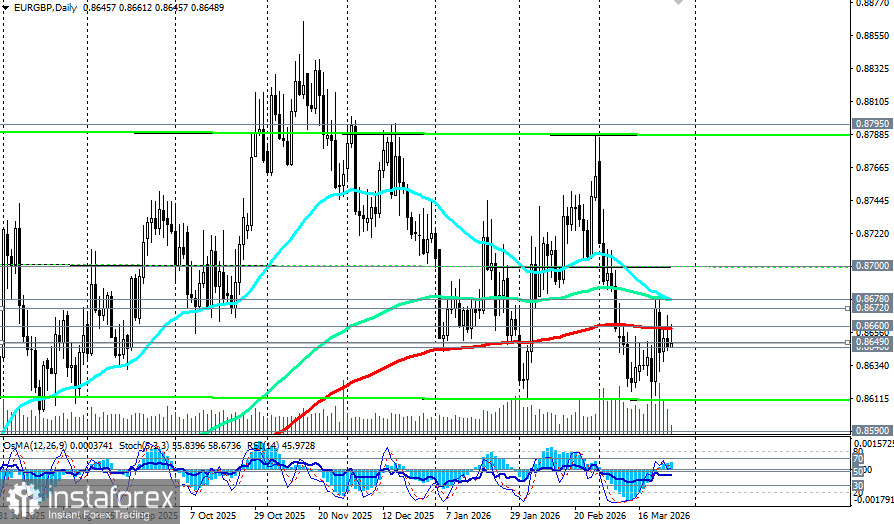

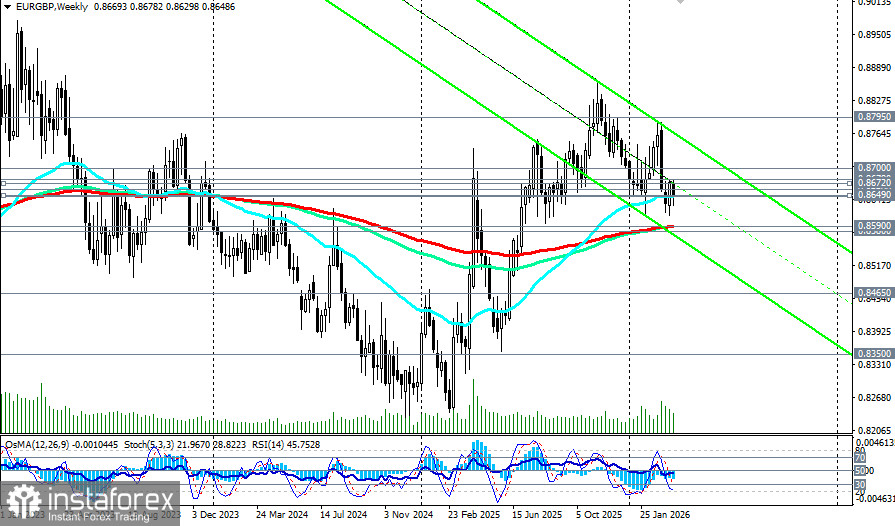

In the early hours of the US trading session on Thursday, EUR/GBP is consolidating around 0.8649 (EMA200 on the 1-hour chart)–0.8646 (EMA50 on the weekly chart), reflecting uncertainty amid escalation in the Middle East and diverging monetary expectations from Europe's two largest central banks. The single currency shows relative resilience, receiving support from hawkish ECB signals, while the pound remains under pressure from stagflationary risks and political instability.

Current situation: diplomatic deadlock

Hopes for de-escalation that emerged earlier in the week after reports of a 15-point US peace plan had evaporated by Thursday. Iran formally rejected the American proposal, denied direct talks with Washington, and set forth its own conditions, including sovereign control over the Strait of Hormuz (see our today's review "XAG/USD (SILVER): structural deficit versus a hawkish dollar").

Media confirm that Tehran stated that Iran will not accept a ceasefire and will not enter into negotiations with the violators.

In response, President Trump threatened to hit harder, and military tensions continue to rise. The US and Israel carry out strikes, Iranian forces launch missiles at Israel and military bases in Kuwait, Jordan and Bahrain, and the Strait of Hormuz remains effectively blocked for the fourth week. This background supports the US dollar and exerts indirect pressure on both European currencies, intensifying risk aversion.

Monetary divergence: hawkish ECB vs stagflationary BoE

A key factor supporting the euro is the ECB leadership's resolute stance. At the "ECB and Its Watchers" conference in Frankfurt, President Christine Lagarde said the central bank is ready to act "at any meeting," and that commitment to achieving 2% inflation is "unconditional." Chief economist Philip Lane stressed that, if incoming survey data prove worrying, the ECB may be forced to raise rates "sooner rather than later."

Governing Council member Joachim Nagel explicitly indicated that a rate hike in April would be an option at the next meeting, should inflation acceleration risks materialize. Market pricing already implies about 16 basis points of tightening in April and almost 65 basis points of cumulative tightening by the end of 2026.

Thus, the ECB signals a much firmer tightening stance than in past energy crises, which makes the euro more resilient.

The Bank of England's position looks significantly more complicated. February inflation data, released on Wednesday, showed headline CPI at 3.0% year on year, while core inflation rose to 3.2%. However, these figures do not reflect March's surge in energy prices.

Deputy Governor Sarah Breeden warned that the current energy shock "differs markedly from the last energy shock in 2022," and that monetary policy should remain steady until the bank has sufficient information on the shock's magnitude and duration.

Unlike the ECB, the BoE faces a more fragile economy. The UK's budget deficit in February was £14.3 billion, the second-largest on record since the Covid-19 pandemic, and public debt remains near 93.1% of GDP — the highest levels since the early 1960s. This increases the economy's sensitivity to rate rises and constrains the regulator's room for manoeuvre.

Economic data: Britain's vulnerability and eurozone on brink of recession

Recent surveys show UK inflation expectations jumping from 3.3% to 5.4% — a 20-year high. This raises the risk of second-round effects via wage indexation, which could force the BoE into more aggressive action even at the cost of slower growth.

Retail sales in February already slowed to 3.6% year on year (from 3.8% previously), missing forecasts and indicating weakening consumer activity.

In the eurozone, data are also worrying. Germany's GfK consumer confidence index plunged to -28 in April — the weakest reading in more than two years. IFO president Clemens Fuest noted that the Middle East crisis "has effectively wiped out growth prospects for the German economy." Yet the market treats these data as a factor strengthening the case for accelerated ECB tightening to combat imported inflation.

Conclusion

EUR/GBP is at the epicenter of a fundamental divergence. The ECB shows readiness for preemptive tightening, treating an April hike as a real option and stressing unconditional commitment to price stability. The Bank of England, conversely, faces a classic stagflation dilemma: inflation expectations have surged to a 20-year high, but the economy is too fragile for aggressive rate rises.

The key zone 0.8600–0.8660 will be the arena of decisive battle in the coming days. Holding above it will keep chances for a move to 0.8700–0.8750, while a break below will refocus attention on March lows.

See more in: EUR/GBP — scenarios of movement on 26.03.2026

Under any scenario, volatility will remain high. Investors should closely monitor the development of diplomatic contacts around the Strait of Hormuz and, importantly, the rhetoric of ECB and Bank of England officials ahead of their April meetings. Success will favor those who can weigh the ECB's resolve to fight inflation against the growing stagflationary vulnerability of the UK economy amid ongoing geopolitical uncertainty.